Two tiers of protection from ERISA claims. One standard your customers can hold you to.

Group health plans are now squarely in the ERISA crosshairs. The Validation Institute's ERISA Immunity Guarantees give plan sponsors a real financial backstop — and give validated vendors a way to demonstrate the integrity that wins serious employer business.

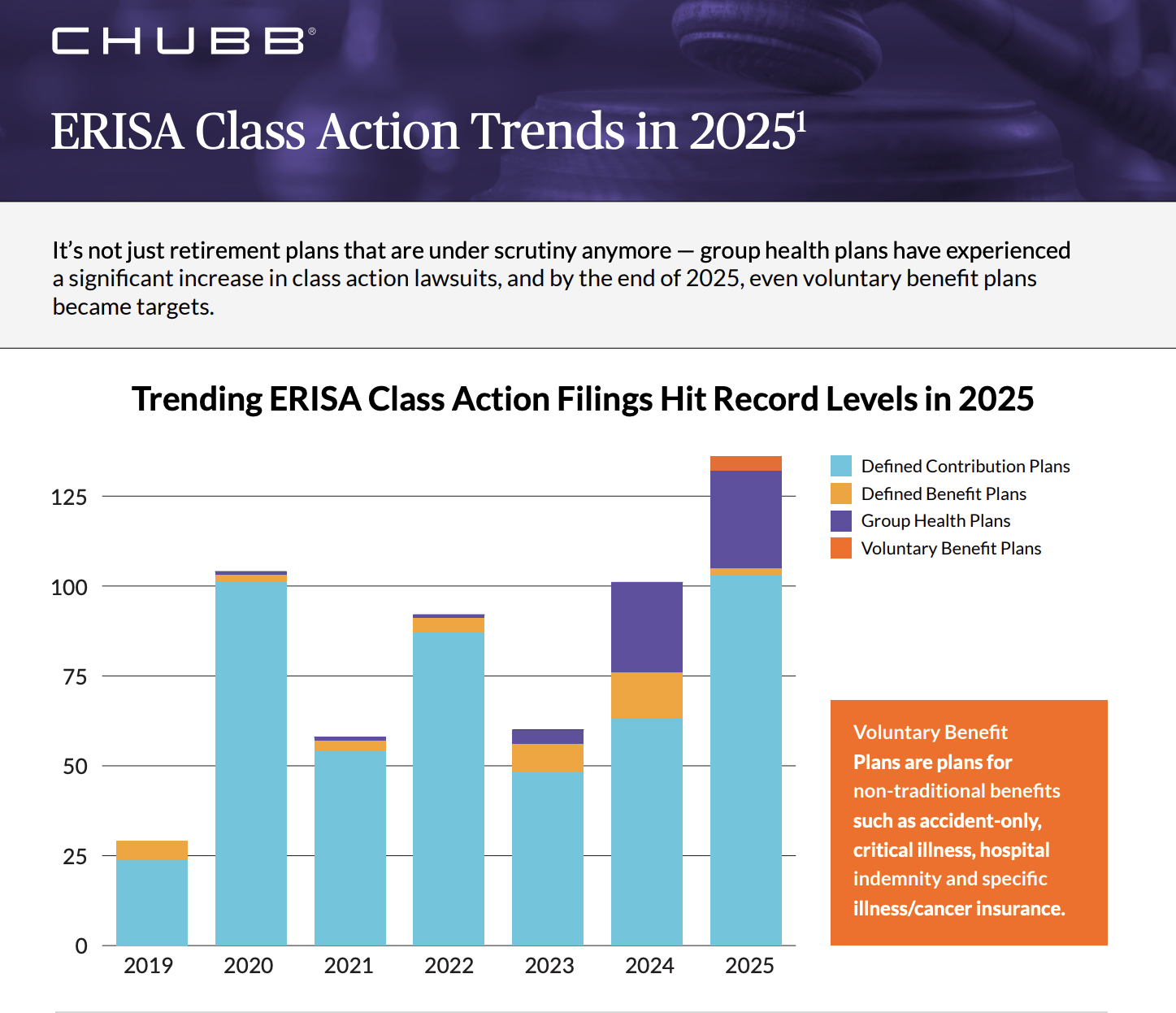

ERISA class actions used to be a retirement-plan problem. They aren't anymore. Group health plans are now squarely in the crosshairs, and 2025 set a record for total filings — with much of the new volume aimed at how plan dollars are managed across PBMs, vendors, TPAs, and advisors.

Plan sponsors are looking for partners that don't add to that risk. Vendors who can prove they manage plan assets like fiduciaries — and who put real coverage behind that claim — win the business.

Source: Chubb, ERISA Class Action Trends in 2025. Reproduced here as third-party industry data; not a Validation Institute publication.

Two Tiers of Protection

Same structure — co-insurance that sits alongside existing fiduciary policies — at two coverage levels and two qualification standards. Pick the one that fits the role you play in the plan sponsor's stack.

Standard tier

$100,000 ERISA Immunity Guarantee

For VI-validated vendors, consultants, and advisors who want to stand behind their fiduciary integrity.

Up to $100,000 in co-insurance coverage

50% of the next $200,000 after the first $5,000

Open to validated vendors and advisors across categories

Covers settlements, arbitration findings, and adjudicated awards

The ERISA Immunity Guarantees aren't limited to one role in the benefits stack. Any organization that handles plan assets and operates with fiduciary integrity can qualify.

Health solution vendors

Care navigation, MSK, virtual care, mental health, advanced primary care, and other point solutions paid out of plan assets.

Third-party administrators (TPAs)

TPAs that adjudicate claims and manage day-to-day plan operations on behalf of plan sponsors.

Pharmacy benefit managers (PBMs)

PBMs that operate as true fiduciaries — independent, transparent, and aligned with plan sponsor interests.

Benefits advisors & brokers

Advisors and brokers who recommend plan design, vendors, and contract terms on behalf of plan sponsors.

Other healthcare players that touch plan assets may also qualify. Schedule a call and we'll tell you whether your category fits.

How Both Guarantees Work

Both tiers function as ersatz co-insurance. The validated entity's existing E&O, D&O, or fiduciary insurer pays the first $5,000. The Guarantee then covers 50% of the next layer — up to $100,000 in the standard tier, up to $1,000,000 in the Platinum tier. Existing insurance covers anything above that.

Because the Guarantee acts as co-insurance, covered entities — and often their plan sponsor customers — can negotiate discounts on their own fiduciary policies. If your current carrier won't recognize it, we'll connect you with a P&C insurer that will.